Payments, Metaverse, P2E games and DeFi derivatives: A deep dive into Fluidity’s use cases

Imagine a protocol — an avant-garde DeFi yield primitive that turns all previous dogma related to earning yields on its head; instead of locking up your assets, users can now earn rewards for every transaction they perform. Now, think of the same platform as an augmentation layer for crypto payments, a troubleshooter across the DEX lifecycle, and a base layer for value transfer in the metaverse; most importantly, think of it as a yield multiplier and system stabilizer for use cases ranging from P2E games, liquidity aggregators, and Maximal Extractable Value (MEV) optimizers.

Welcome to the world of Fluidity Money. First, a short primer on Fluidity’s many moving parts. If you are in possession of stablecoins like USDC, you can exchange them for fUSDC (fluid asset USDC) — a wrapped form of the stablecoin — on the Fluidity platform.

Where it differs from other DeFi yield systems is that you earn rewards on your fluid assets by using/utilizing them — that is, if you send them, receive them, swap them, or trade with them, you stand a chance to earn randomly paid yields and “large dividends” which can range from cents to millions. This is the polar opposite of traditional methods, where you have to lend, stake or lock up your assets in an idle form for an extended period of time to earn yields.

Fluidity, on the other hand, envisages you, as a user, earning rewards through everyday activities like payments for food, rent, or interactions with your favourite decentralized exchange (DEX) or NFT marketplace, or blockchain gaming platform.

If User A transfers a fluid asset like fDAI to User B, both the sender and receiver stand the chance to earn rewards, split 80:20. 40–70 per cent of all transactions will be yield-bearing.

The utility structure of Fluidity is clear. But, what were the biggest lacunae in the current crypto incentive structure that Fluidity is solving? The yield farming and liquidity generation paradigm in this DeFi epoch is highly unsustainable. Take the case of liquidity mining, where protocols announce mining programmes to attract users to provide liquidity with the promise of high APYs. Over time, as the resources decay and the actual rewards revert to mean, the same users will fan out in search of higher APYs elsewhere. That is, the protocol will be paying over the odds for liquidity devoid of stickiness and a user base not incentivised to explore the protocol. In addition, liquidity mining disproportionately rewards high-capital users who corner a large percentage of the APYs.

That is where Fluidity’s Transfer Reward Function (TRF) comes in, in the form of Utility Mining. Its purpose is to reward genuine users of the protocol, paying them with governance token rewards on top of the usual TRF rewards if they display intended behaviors. Let us consider an example.

If DODO signs up for Utility Mining, and a user performs a designated transaction with an fDAI on DODO, the user could stand to win up to three types of yields: TRF rewards, Fluid governance tokens, and DODO governance tokens.

With Utility Mining, protocols can advertise a higher yield, and, by extension, attract the highest user attention. To control Utility Mining emissions, utility gauges are in place — Fluidity DAO users and protocols with power to vote on emissions can decide which platform receives the highest emissions. Think Curve Wars (fight for the flow of liquidity in DeFi), and extrapolate it to a competition to control the flow of users across chains and protocols; here, liquidity is just the second-order effect of utility. On a high level, Fluidity is an incentive layer that gives protocols a chance to bid for the attention of highly engaged users who are aligned with the overall vision of the protocol.

Now, let us analyze Fluidity’s many different use cases in detail.

1. Fluidity as a payments booster layer

From Bitcoin ATMs in North America and Spain, to small vendor settlements in South and East Asia, cryptocurrencies in retail payments have come a long way since the first Sats were used to purchase pizza in May 2010. AXA Insurance in Sweden now allows customers to pay in BTC (although they don’t hold crypto in their balance sheet). So does Starbucks. Gucci now accepts BAYC’s Apecoin. Crypto.com, Gemini and Coinbase have all integrated with Google Pay. In addition, there are clear indications that, among retail merchants, there is a growing interest in crypto as an alternative payment rail. A June 2022 survey by Deloitte and PayPal revealed that around 75 percent of retailers across the world plan to accept cryptocurrencies within the next two years, and more than half of them have sunk over $1 million into infrastructure facilitating those payments.

The keyword here is scale-agnosticity. Big, small and medium-size retailers alike are interested in this space, and willing to put their money where their mouth is. In addition, there is a lot going for crypto in payments. There is transaction finality, which translates to better cash flow management for the retailer. It is cheaper. And, it is much more accessible for large parts of the world. On the flip side, retailers will have to make an initial investment on infrastructure (revamped PoS terminals etc), and will often have to deal with opaque and mercurial tax regimes.

So, where is that last-mile stimulant for mass adoption coming from? Enter Fluidity. Currently, there is a major misalignment of incentives on both sides of the payments market. Crypto owners have no reason to spend their tokens — it is much better to stake and earn rewards, or plain speculative hold. Merchants see no direct advantage in accepting crypto as payment. Fluidity sweetens up the deal for both the parties involved. Spenders, as we mentioned above, can earn TRF rewards ranging from cents to millions merely by putting their crypto to work. Merchants, merely by accepting the fluid tokens, put themselves in the running for 20 percent of the rewards. This is opportunity cost, redefined.

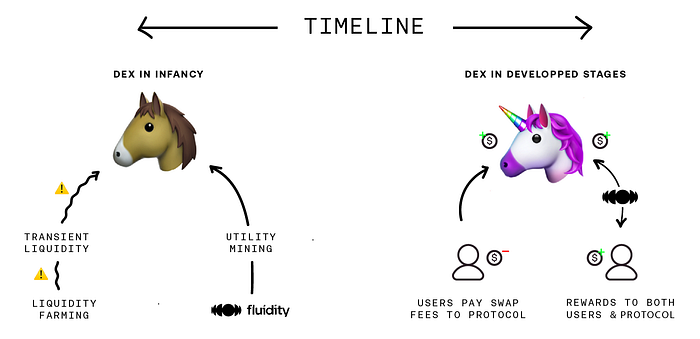

2. Fluidity as the DEX doctor

Fluidity solves a whole host of issues across a decentralized exchange lifecycle — right from the teething liquidity problems at inception, to the latter stages when questions emerge on platform revenue, value accrual and sustainability pathways.

Bootstrapping liquidity is one of the biggest issues faced by any fledgling DEX. By signing up for Fluidity’s Utility Mining campaign, a DEX can offer higher yields than its rivals (with Fluid governance tokens on top of the usual liquidity mining rewards) to attract LPs and incentivize users to explore every nook and cranny of the protocol. The platform also need not focus solely on attracting LPs; they can also build up a high-quality, sticky, active and engaged user base, and ensure fairness in token distribution.

Now, let us take an established DEX like Uniswap and figure out where Fluidity can help. Most recently, a polarizing governance proposal had mooted the partial activation of a “fee switch”. The platform levies a 0.3 per cent trading fee, and the revenue is distributed as LP rewards. If the fee switch is implemented (in select pools initially), 0.05 per cent of the LP revenue will be diverted towards the holders of the governance token UNI. This would bolster the UNI treasury, which can then be used to fund protocol-owned liquidity (POL) and grants for ecosystem developers.

However, the fee switch, which basically siphons off LP rewards, can be a double-edged sword. Liquidity providers, already operating under razor-thin margins and half of them suffering net deficits because of Impermanent Loss (IL), could leave the protocol if they descend further into the red. This could reduce depth of liquidity, and bring down the platform dominance in the market if users migrate to other DEXs which offer better prices.

The big question remains. Why would a DEX as dominant as Uniswap, facing no revenue crunch whatsoever (check out this Dune query), be involved in such a risky maneuver? They could LP in their own pools, which would deepen protocol liquidity and bring in additional revenue. But, the simple answer is that such a move wouldn’t suffice. Even platforms at the very top of the food chain are in search for new (if unorthodox) revenue pathways, with competitors circling closer to the throne. Everybody from Curve to Orca, Sushi and Quickswap are building their own versions of concentrated liquidity platforms, and can easily undercut Uniswap’s winning model under the right conditions.

Fluidity can provide sustainable alternatives to such a scenario.

As we explored in detail in this piece, Uniswap can explore hybrid solutions with Fluidity. The fee switch can be turned on and LP fees diluted in some of the more efficient pools; in others, Uniswap treasury revenue can be bolstered through the induction of Fluid assets.

Take the case of Uniswap. If 10 percent of all transactions on Uniswap would be done with a fluid asset in it, and 30 percent of the payout goes to the receiver, the treasury would receive an annual revenue of around $1,000,000. Keep in mind that the revenue could be much higher after taking into account the large payouts.

3. Fluidity to augment NFT marketplaces

Imagine this scenario. You scrimped and saved for the day that you would finally be able to afford that elusive droopy penguin jpeg on OpenSea. You watched with trepidation as the NFT floor price jumped from just a couple of hundred dollars to hundreds of thousands over the period of just a few months. You waited patiently, keeping tabs on every cycle for a suitable entry. In May, the perfect time to snipe presented itself.

NFTs are a burgeoning economy, with sales hitting $42 billion dollars in the first seven months of 2022, even amid a global macroeconomic slowdown, compared to $40 billion in the whole of 2021. With fluid assets, NFT collectors stand a chance to earn life-changing TRF rewards for every purchase made. That is, the mere act of buying the penguin jpeg that you always wanted could land you anywhere from $0.1 to $100, $10,000 and $1 million. On the flip side, NFT marketplaces are incentivized to accept fluid assets with 20 per cent winnings from the reward pool. The yield grows exponentially higher in the case of fractionalized NFTs — as more people dig their forks in the pie, so does the reward quantum and probability.

4. Fluidity as base layer for the Metaverse

If one were to try and plot out an idealistic vision for the emerging metaverse economy, the major coordinates in each quadrant would be: on-demand, creator-led, peer-to-peer open-source, and participatory. The sector, poised to grow at an incredible CAGR of 13.1 per cent over the next couple of years, reimagines all human interactions in the physical space extrapolated to highly interoperable virtual realms operating on pre-defined social contracts that users can opt into. Now, you can buy parcels of land in a finite space, take a jog downtown, visit a gallery, attend a concert, enjoy a day out at the beach — anything that can be done within the constraints of atoms, the bits can reproduce, and more.

With DeFi as the financial backbone and NFTs as the ownership layer, imagine the millions of interactions — the exchange of values — which would happen on a daily basis in one single system. Now, think of a thousand such metaverses, all with bustling internal economies and cross-pollination across digital jurisdictions.

The sheer scale is difficult to fathom.

What responsibilities would the base economic layer of such a system be expected to shoulder? First and foremost, it should uphold the foundational principles of decentralization and fair value transfer. Second, it should ensure a healthy economy, where money is mobile and in circulation, and hoarding and speculation are discouraged with the help of carefully laid out incentives.

This is where Fluidity comes into the picture.

Q: Can it backstop any descent into asset hoarding and speculation? A: The novel TRF lays down the foundations of a ‘spend-to-earn’ DeFi economy.

Q: Can it incentivize interoperability between different worlds?

A: Fluidity is a chain-agnostic incentive layer designed to enable seamless value transfer.

Q: Can it ensure avenues for fair and equitable distribution of resources?

A: Utility Mining. Check.

On a macro level, metaverse is a frontier technology. And, frontier technologies favor asymmetric bets — which is exactly what Fluidity offers. Imagine Metaverse A where the financial system is integrated with fluid assets. That is, every single interaction that you perform gifts you a chance to earn (asymmetric) rewards. Now imagine Metaverse B, which is non-Fluid in nature. Everything else the same, users have an added incentive to flock to Metaverse A. In the larger picture, this enables economies of scale to exponentially pop up across the board.

5. Fluidity as a brand new derivative product

The traditional derivatives industry was unimaginably disrupted in the ascendance of DeFi. For the first time ever, avenues opened up for regular users to get access to complex, high-yield options strategies that were dependent only on the volatility of underlying asset prices and catering to a spectrum of risk preferences. Fluidity is the next iteration in the world of decentralized derivatives, a one-of-a-kind primitive opening up the industry to a very different type of yield.

Let us run through the basics first. Options is a contract between two parties — a buyer and a seller. The contract runs on top of an underlying asset, and essentially makes bets on its price action. That is, you are not dealing with the underlying asset in itself (be it ETH or BTC or stocks), but earning yields from its price volatility. Unlike stocks, most options operate within a timeframe, with an expiry period. After the expiry date, be it in days or months, the options contract becomes worthless. There are two main types of options available in the market: Call and Put. A call option basically gives the purchaser of an options contract the right (but not an obligation) to buy the underlying asset at a specific price. A put option, on the other hand, gives the purchaser the right (again, not an obligation) to sell an asset at a predetermined price.

Since the contract is skewed in favor of the options buyer (who can choose whether or not to exercise the contract), the advantage is offset with the seller being paid a ‘premium’ upfront for access to the call or put contract.

Then there are the perpetual futures, a speciality of the crypto derivative markets; here, unlike all the contracts we have explained so far, there is no expiry date. So, a trader can hold on to a position as long as he likes. That opens up a slew of possibilities.

In that vein, you can think of a fluid asset transaction as a ‘spot options contract’ variant — both the buyer and seller stand a chance to earn a potential premium in return for asset utilization. Let us go into it a bit deeper. When you swap your fEth for USDC, you are relinquishing your exposure to the asset and selling the potential upside in return for a possible ‘premium’ (80 per cent of the TRF yield, which accrues to the sender side of the transaction). The counterparty in this case, buying exposure to the underlying asset, also earns the potential premium, albeit at a discount (20 per cent of the TRF yield, which accrues to the receiver side).

Check out Dopex, a decentralized options exchange where anyone can buy and sell options in an easy-to-use interface. And their documentation.

6. Fluidity as a non-invasive solution to P2E woes

The concept of Play-to-Earn games first emerged in public consciousness with the rise of Axie Infinity, a Pokemon-adjacent blockchain game that took Philippines and Southeast Asia by storm in the middle of the pandemic, rising to an over $3 billion valuation by October 2021. In the early days, native Axie tokens became yield-bearing instruments of such value that it became a significant medium of exchange in the Philippines, sometimes superseding its official currency. Currently, however, the game is facing a trial by fire — its Ronin chain was hacked to the tune of $650 million, the global macro inexorably worsened, and glaring flaws in its economic structure were exposed for the world to see. Its native utility token Smooth Love Potion (SLP) is on a downward slide, new user growth has stalled, and even its founder Sky Mavis has admitted to a rethink of the game’s foundational model. Google trends show that interest in Axie Infinity has plummeted in the Philippines (the largest market), and datasets show that an average Axie scholar earns less than the minimum wage — a sharp correction over just a few months.

While it would be unfair to single out Axie, its woes — as the first mover in the field — make for an interesting case study. Axie has a toxic dependency on new users who need to keep coming in to keep the system functional; what we see now is that once the flow has stemmed, the model looks ready to collapse.

Fluidity can be a non-invasive solution to a lot of P2E’s problems, a yield multiplier and a system stabilizer. For the players, transactions with fluid assets would equate to enhanced payoffs; for the gaming platform (earning a cut of TRF rewards), this could be a sorely needed revenue boost. Just to comprehend the scale of what we are talking about, Axie Infinity alone recorded $3.5 billion in NFT transactions in 2021. The platform needs only capture a fraction of that value.

7. Fluidity in MEV extraction

When you submit a transaction on the Ethereum network, a non-zero amount of time will elapse before it is confirmed on the blockchain. Your transaction, while it is publicly visible on the mempool and awaiting confirmation, can be simulated by bots to see if there is a net positive change in its aftermath. For example, if your wallet balance increases after a successful arbitrage, these bots will attempt to frontrun you by submitting an identical transaction (only under its own wallet address) with a higher gas fee to outbid you on the block.

Let us analyze a different case. If a bot sees a $1 million Eth buy order on the mempool, it makes a reasonable assumption that the price of the asset will moon in the immediate aftermath of the purchase. The bot will then launch what is called a sandwich attack, frontrunning the Eth purchase order with a similar transaction of its own and then selling the ether tokens after the $1 million buy order has been filled.

Let us look at one final example. When a user takes out a loan on a lending protocol, the position is always over-collateralized — that is, the user is expected to post collateral in excess of the loan being taken out. If the value of the collateral falls below a threshold, and if it is not reinforced on time, the DeFi protocol allows anyone to liquidate the loan position to maintain system solvency; liquidators (bots) are incentivized with a fee or a portion of the collateral.

All the above are examples of a phenomenon commonly known as Maximal Extractable Value (MEV), or the net positive value that leaks out of the system and aggregates in its crevices. MEV is also often referred to as the Miner Extractable Value as block producers (who can reorder transactions in ways that benefit themselves) and sophisticated bots are the two entities monopolizing the space, leaving little to no benefit for either the users or the protocols whose actions generate the value in the first place.

This zero-sum game is changing now, with the emergence of protocols like Rook.fi on Ethereum and Jito Labs on Solana, all working towards a democratization of the MEV extraction space.

Let us take the case of Rook.fi, and analyze where Fluidity comes into the picture. The protocol’s foundational belief is that MEV should accrue, not to the miners, but the originator of the transaction or the protocols that created the MEV in the first place. For that, the platform uses Keepers — sophisticated bots that survey the state of the blockchain and compute all the different possibilities in order to identify transactions that result in profit. A user can route his transaction through the Rook RPC; this transaction will be auctioned off to a whitelisted keeper, who will then execute the order and share any resulting MEV profits with the user and the protocol. In essence, the user gets his order filled with zero fees, and even earns an extra yield on top of it.

Let us consider a real-life example. Suppose an order comes in through the Rook RPC for $1,000,000 worth of ether token purchase from a Uniswap pool. This will, in all probability, cause imbalance in the pool and open up arbitrage opportunities with, say, Sushiswap. The keeper who wins the auction can complete the transaction, and, in tandem, extract the MEV in the form of the arbitrage opportunity. The user gets $1,00,000 worth of ether tokens, and an additional $100+ as MEV yield.

This is where Fluidity comes into the picture. If the keeper performs the arbitrage trade by involving a fluid asset in the transaction, it can boost the yield manifold and benefit all parties involved — the keeper, the user and the protocol.

8. Fluidity to supercharge your arbitrage trades

Crypto assets worth billions of dollars are traded every single day. Arbitrage traders take advantage of the volatility and pricing imperfections, exploiting different values for the same asset across different markets. Take a hypothetical scenario: Sol is trading at $38.7 dollars on Binance; On Kraken, its value is $40. That means, a trader can purchase Sol via Binance and sell it on Kraken for an instant 3.36 percent profit.

Arbitrage is a game of razor-thin margins, especially on high gas fee chains like Ethereum. In such circumstances, Fluidity and the TRF yield could provide a much-needed cushion to supplement existing gains. Also, the higher the gas fees on the chain that the Fluid assets are being used, the higher the expected reward outcomes (albeit capped).

In a detailed article found here, we have identified a particular arbitrage scenario where the net yield can go up higher than 70 percent on the introduction of fluid assets.

At the same time, it is important to note that Fluidity payouts don’t scale with transaction size; however, a useful corollary would be that the rewards compound with the frequency of transactions. What this means is that the higher the number of transactions and swaps a user performs (arbitrage traders trade at a much higher rate), the much higher the probability of earning a large dividend in Fluidity’s gamified system.

9. Fluidity as a sustainable liquid-staking alternative

The Ethereum Merge is hovering on the horizon. Soon, Layer 1 will shift from a Proof-of-Work (PoW) consensus system to a Proof-of-Stake (PoS) mechanism where validators who stake their ether will produce the blocks in return for rewards and any additional MEV. The threshold to become a validator is quite high — you will have to pledge at least 32 Eth. Alternatively, users can pool their Ether and ‘delegate’ it to a validator who will run the node on their behalf.

Enter liquid staking derivatives (LSDs) like Lido and Rocketpool which stake Ethereum on the Beacon Chain on your behalf, and, unlike static staking systems — which lock up your assets indefinitely — reward the user with native ‘liquid’ tokens representing your share in the pool. That would be stETH from Lido and RETH from Rocketpool. These tokens can, in turn, be staked with other DeFi protocols to earn secondary yield.

Lido is currently leading the race with more than $6.9 billion in total value locked, according to DeFi Llama.

While initially considered the next best thing since sliced bread, LSDs are currently under massive scrutiny for its capability to undermine the entire Ethereum network post-Merge. In a detailed post, researcher Danny Ryan from the Ethereum Foundation highlighted the possibility of Lido and similar protocols emerging as a “stratum for cartelization and induce significant risks to the Ethereum protocol and to the associated pooled capital when exceeding critical consensus thresholds”. That is, if Lido emerged as the choice platform to stake a majority of Ether tokens in circulation, “then the token holders [delegators] can force cartel activities of censorship, multi-block [maximal extractable value], etc, or else the [validator] is removed from the set. If pooled stake under one LSD protocol exceeds 50 per cent, this pooled staked gains the ability to censor blocks,” Ryan wrote. That would be nothing short of an existential threat.

Many big names, including Ethereum co-founder Vitalik Buterin, asked the LSD protocols to self-limit and control its share of stake on the Beacon Chain.

Enter Fluidity, the new and improved avatar of liquid staking. If a user deposits ether tokens into Fluidity, the yield is reflexive — you can transact or swap with your Fluid assets to earn TRF rewards, or you can choose to stake/LP fEth on to earn rewards on top.

Also, unlike other LSDs, cartelization is not an inherent vulnerability as far as Fluidity is concerned; in fact, it is a feature and not a bug. The gauges that control Fluid governance token emissions are designed to be fought over by protocols — an incentive layer that gives protocols a chance to bid for high-quality user attention. You can read all about the Fluidity governance structure here.

10. Fluidity for liquidity aggregators

How does a liquidity aggregator, like Solana’s Jupiter protocol, work? Think of a travel aggregator in Web2, which combs through multiple portals to offer users the best possible deals. Now, extrapolate that definition to a protocol that trawls through DEXs, automated market maker (AMM) pools and order books to route the best possible deals on token prices for the users. How does the protocol decide the best route for trades? Currently, it is calculated off-chain because the process is really time-consuming and expensive — involving multiple ‘hops’ across DEXs to exploit the optimal pathway.

Jupiter currently supports 2-hop routes — to complete a USDC-SOL, Jupiter goes through intermediaries like mSOL (marinade liquid-staked SOL), all the routes ranked by the ones that give the most tokens in return.

Where does Fluidity come into the picture? One of the factors that Jupiter’s routing algorithm optimizes towards is the best expected value at the end of the route. That is, maximizing the best possible outcome for the user. Now, let us say Jupiter aggregator introduced fluid assets throughout the routing process. The more fluid assets are introduced, the higher the probabilities attached to earning yield. One interesting possibility is that users could start to consider where and how fluid assets are routed (for additional gains), and mark their choices accordingly. Eventually, Fluidity governance can endow specific DEXs and protocols with a higher probability of yield with every transaction.

Fluidity as a utility layer for stablecoins

When Terra’s doomed UST stablecoin first launched, its meteoric rise came on the back of Anchor Protocol, which provided a fixed yield for UST deposits at a very attractive and fixed 20 per cent APY. The perennially high yields were backed by the reserves of non-profit Luna Foundation Guard (LFG), with backing from market makers like Jump Crypto. That is, the demand for UST was sparked almost exclusively by the Anchor Protocol — more than 50 per cent of circulating UST was deposited in Anchor, making the protocol the biggest UST sink.

At the end of the day, it was Anchor that turned out to be the fulcrum of Terra’s undoing. The artificially propped up 20 per cent APY was not sustainable by any stretch of imagination, and the chain collapsed before it could organically develop an alternate source of demand.

Stablecoins have a utility problem, which needs to be an organic solution. That is where Fluidity shines. Think of it as a utility bubble for stablecoins — TRF rewards create an incentive for stablecoins to be used and moved and swapped, with Utility Mining rewards an additional layer of yield on top. Moving the assets around also helps hedge against speculation to a large extent — along with incentives for money to be used the way it is designed to be used.

Visit us to learn more:

https://t.me/fluiditymoney

https://discord.gg/w9DVhGDR

https://twitter.com/fluiditymoney